Do you ever USE your Emergency Fund? What for?

We all know it’s smart to have money saved up for emergencies, but what exactly constitutes an “emergency” these days? And do you ever feel bad when pulling from it even when emergencies DO come up?

(I do!! Which makes no sense at all since it’s literally what they’re set up for!!)

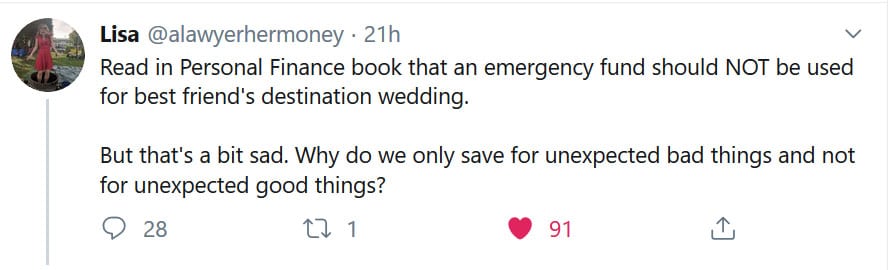

Been thinking about this a lot since my girl Lisa dropped a bomb on Twitter:

Interesting, right?!

My first reaction was: “Nope! That’s a “want” and not a “need” – don’t even THINK about tapping it, missy!!” But the more I pondered it the more I became uncertain of my answer…

Maybe it is fine to tap if the money’s there and it’s super important to you? Wouldn’t it be better than going into debt or liquidating other funds? And who’s making up all these “rules” we have to follow with this stuff anyways?! There’s no money police!!

After a while I forgot about this and went about my day, but a little later it crept back in and I hopped into the comments to see what others were saying.

Here were some of the highlights:

- “I think a separate fund is best for that. The emergency fund is usually branded as the medical or job loss fund.” – @LittleDollar

- “I would recommend NOT using an emergency fund for a wedding but trying to “cash- flow” it. Doesn’t mean you shouldn’t go to the wedding you just have to pull the money from someplace else” – @adimesaved

- “The wedding most likely wouldn’t be a surprise so therefore not an emergency, if it is a surprise than does says friend expect everyone to drop everything to jet off for her suprise destination wedding?” – @Charlotte_Musha

- “I think it’s your money, and nobody should tell you how to spend it. What is the point of a wealthy retirement if you only start living life then? I say you create a plan and figure out how to make it to this memorable event!” – @MetanoiaTraject

- “I recommend folks write a list of what expenses they consider an emergency when starting their emergency fund. So when something happens you don’t have to question if the expense counts. However, I also recommend folks have a vacation fund too. So you can do trips on the fly.”

– @purpose_money - “Debt free already?? Using the fully funded 3-6 months emergency fund? If so, why not. If in debt and using that emergency fund…no way.” – @moneysavvydaddy

- “Oh! I wrote about this. I have an Urgency Fund for “YOLO-Emergencies” like this: https://www.frugalityandfreedom.com/urgency-fund/” – @FrugalityFreedm“

- “The problem I have with my emergency fund is I don’t want to use it for “normal” emergencies. It’s gotten to the point where it has to be “a hurricane destroys my house at the same time as I lose my job and car” type of emergency for me to touch it. (I have a problem!)” – @Jovermyer1

- You can have as many savings accounts as you wish these days! I suggest naming them fun things like #FinancialFreedom fund, Escape to Bali fund, #SkiBumSavings #Sabbatical so the transactions represent your goal, as opposed to deprivation – @TwightFinancial

- And then my favorite response by @skostarasRV:

Haha…

But perhaps @NinjaBudgeter came up with the best solution of all:

Let’s start calling it an ‘unexpected fund’.

This draws a much clearer distinction on when you can tap it and when you can’t, all the while covering both the *positive* and *negative* items that pop into our lives as they do. Of course, you’d also need to top it off even MORE in this case since it would now be covering two large areas (with one being much more tempting to activate, let’s be honest!), but an interesting solution to the quandary indeed.

Personally, we go back and forth with having an E Fund or just mixing it all together into one main pot as we’re currently doing, but I think over time you get better at learning how you operate and what barriers need to be in place (or not) in order to maintain that healthy balance. Stacking up cash to never touch again isn’t that helpful, just like liquidating it down to zero constantly isn’t either. It always takes some fine tuning until we learn what’s best for us!

At any rate, more food for thought this week…

How do you guys currently manage your E Funds? Are they off limits to anything but hurricanes and heart attacks, or do you allow yourself to pull from it during emergency *wants* too?

Of course, step #1 is simply *having* an emergency fund set up to begin with, so if you’re still working towards that just keep on stacking and worry about all these “problems” later 😉 Once you’ve got it filled up the main battle has already been won!!

-

Bad Excuses to Spend Money 🤷️

What’s even worse than enjoying your close friends invest cash on crap ...

![]()

The Rubik theme is the best Premium WordPress Themes that perfect for news, magazine, personal blog, etc.